TL;DR

Fork Liquity Protocol to build a decentralized stablecoin (Threshold USD - thUSD) purely backed by tBTC. Make Threshold DAO owner of the protocol and distribute profits through T buybacks and/or PCV.

This is a way to generate profit for Threshold Network while simultaneously encouraging adoption of tBTC by making it a collateral that can be borrowed against.

Introduction:

Liquity Protocol launched in April 2021 and is a decentralized borrowing protocol that allows you to draw interest-free loans against Ether used as collateral. Loans are paid out in LUSD (a USD pegged stablecoin) and need to maintain a minimum collateral ratio of 110%.

In addition to the collateral, the loans are secured by a Stability Pool containing LUSD and by fellow borrowers collectively acting as guarantors of last resort.

Here’s a quick overview:

Whitepaper: https://docsend.com/view/bwiczmy

Documentation: https://docs.liquity.org/

Why?

In order for tBTC to become an attractive wrapper for BTC it needs use-cases. Integration with existing platforms are important, but so is looking for alternative ways to expand the tBTC ecosystem on its own.

Decentralized borrowing with BTC collateral on Ethereum is hard to come by. Some platforms allows you to borrow against WBTC, renBTC etc, but these wrappers suffer from various degree of centralization. The most popular wrapper (WBTC) custodies funds and operates minting/unminting process via a multisig federation. This degree of trust is not acceptable to many bitcoin holders. Solving the trust issue will allow more people borrow against their BTC.

Furthermore, these platforms generally offer variable interest rate and this results in uncertainty for borrowers because interest rates are highly dependent on market conditions. Because of this, long-term loans (e.g borrow to buy real estate or other “real-world” assets) becomes risky and difficult to maintain.

Interest free loans backed by tBTC collateral will enable bitcoin holders to borrow against their BTC in a trustless manner, without involvement of custodians or similar forms of centralization risk. Liquity Protocol is “pay once” (issuance fee starts at 0.5%) and borrow for as long as you like.

Given that a stablecoin (Threshold USD - thUSD) will be minted, this use-case also enables a purely decentralized stablecoin 100% backed by BTC - itself a very attractive prospect.

There is a fee of minimum 0.5% for each loan, and there is a minimum fee of 0.5% for redemptions (don’t worry, paying back your loan is always free - redemptions is people exchanging thUSD for tBTC).

Parts of the profits from usage of the protocol can be distributed to Threshold Network, thus giving us an additional income stream for T DAO.

Liquity Protocol is immutable, it cannot be altered. This is a “set and forget” type of platform. We pay the cost of development once and reap the reward forever. Liquity Protocol has been battletested well, at one point topping $1.5b LUSD in circulation.

source: Liquity

The single largest known actor (Justin Sun) at one point had a deposit of 669,000 ETH in the protocol:

The team behind the Liquity Protocol has carefully tested and audited the protocol to perfection. It’s both a solid project and team.

Forking the project should be fairly simple and only involve minor changes to fit our needs.

How can Threshold Network profit?

In Liquity Protcol, a token “LQTY” is distributed to depositors in the stability pool. It’s akin to liquidity mining / yield farming. Deposit LUSD into the pool and get paid LQTY rewards. The higher your % of the LUSD in the pool is, the higher % of the LQTY you will be farming.

The token distribution is ongoing for 35 months with a max supply of 100,000,000 LQTY. No further LQTY will be issued.

The chart above show issuance for the first 35 months. The rest of supply (~70M) is mostly reserved to initial investors & team.

Once 100M is minted the stability pool will not earn any LQTY, but the stability pool still present an opportunity to profit:

Whenever a user is liquidated (110%) the stability pool (which consists of LUSD) uses LUSD to buy the collateral (ETH) of the user at discount (~10%). By withdrawing the ETH and selling it on market, this can result in up to 10% profit for each liquidation.

The stability pool of Liquity shares many characteristics with coverage pools implemented in KEEP, and later Threshold Network. The funds are in both cases used to cover liquidations. This is arguably a much better design than auctions that are both unreliable and costly during times of high market stress, it yields a high degree of predictability and margin of safety that are not easily accomplished the auction way. Even though I do not make this a part of current proposal, it might even be that stability pool and coverage pool can be combined for maximum capital efficiency.

The LQTY token, when staked. earns profit from all loans and redemptions. Someone borrows $1,000,000 ? The protocol makes (at minimum) $5000. That profit is then split among all LQTY staked.

E.g if there is 100,000 LQTY total staked and you have personally staked 1000 LQTY, a loan of $1,000,000 will result in ($5000 / 100,000) * 1000 = $50 LUSD being added to your personal account.

However, when you really think about it, the LQTY token is just bloat. It serves no purpose other than incentivizing the stability pool growth early on. Once it’s no longer issued, it becomes a drain on the system. Profit from lenders are distributed to passive LQTY holders (whom provide no additional value to the protocol).

Yes. In this proposal, I suggest to eliminate the LQTY token altogether and replace it with a different mechanism:

Without LQTY token, we have several new options on how to split profits form the protocol:

- Stability pool

- T-token buy backs

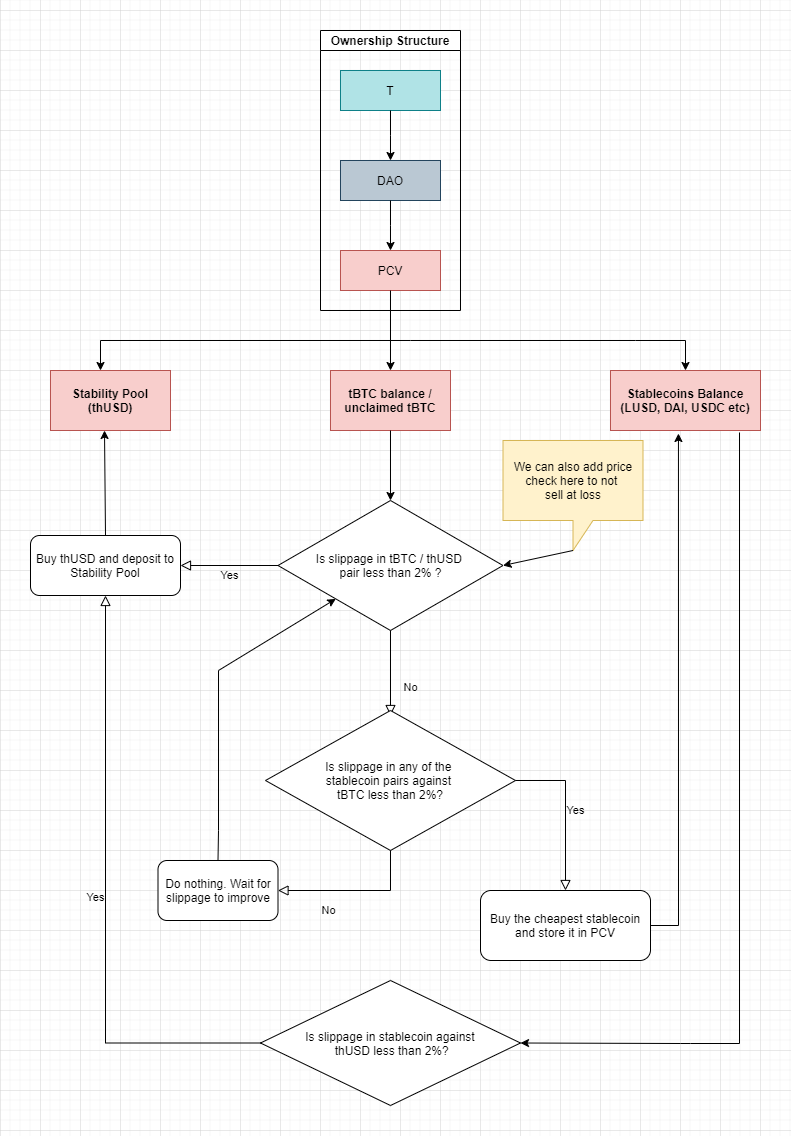

- PCV (Protocol Controlled Value - T DAO owned funds deposited in the stability pool)

By distributing profits into the stability pool, we can ensure that the long-term sustainability of the protocol is maintained. Liquity Protocol assumes that the liquidation rewards (~10%) is enough to maintain the pool, and that may very well be true, but having an additional profit stream into the stability pool will give us another layer of security.

How much % should be sent to the stability pool is up for debate and can be controlled by the T DAO. It might be worthwhile to implement a hardcoded minimum %, but beyond that it can be adjusted by the DAO to fit our needs. E.g: if there’s not enough funds in the pool, we vote to increase the % of profits going into the pool and vice-versa.

Depositing profits into the stability pool is in essence “renting liquidity”: The more profits is sent into the pool, the more liquidity we can expect it to contain. There’s an equilibrium to aim for (an amount of funds that will be sufficient to cover liquidations during big crashes / black swan events), beyond that, it’s wasted capital. If we find that the pool is large enough, the rewards can be reduced and vice-versa.

However, renting liquidity means we have to keep paying. We may decide that Protocol Controlled Value (owned liquidity) is better than distributing profits into the stability pool (rented liquidity). I personally believe this may be an even better and more exciting option because T DAO will retain ownership and continue to control the pool liquidity. With rented liquidity we have no control over the pool and there may be times, such as under high marked volatility or black swan events that pool liquidity vanishes and where even increasing rewards will not be sufficient to bring the pool liquidity back.

If we want to go with PCV, this can be accomplished either in combination with the above or by simply by abolishing stability pool distribution altogether and direct profits (thUSD) into the PCV’s stability pool position. If we do this, it should be further automated with selling of liquidated tBTC for more thUSD or other stablecoins (B-Protocol already does this - maybe we can fork their system?). That way the PCV will continue to grow over time and create a large buffer for the protocol.

The T-token buybacks is where Threshold Network holders will directly benefit from this proposal. It will help increase value of Threshold Network anytime a loan is drawn or a redemption is performed. Profits distributed as thUSD can be automatically converted to T which is then burned. This will result in consistent upward price-momentum as long as the lending protocol is in use.

Additionally it helps to preserve the thUSD peg given its soft-ceiling and hard-floor that naturally draws it to the upside and in need of some downward pressure.

But we need to bootstrap the protocol

LQTY token serves that purpose, without it, it will be harder to bootstrap the pool. When Liquity Protocol launched, the pool had tens of millions of LUSD within hours. We want to accomplish something similar, without the LQTY token.

There are some options:

- Distribute 100% of profits into the stability pool for the first 3-6 months to encourage liquidity

- Buy tBTC from the sale of T, lock tBTC as collateral on the platform and borrow thUSD. Place the thUSD into the stability pool.

- Direct 100% of profits into the PCV and hope people use the platform enough to build a PCV.

- A combination between 1 & 3

- Direct T rewards to the stability pool (just like how T DAO directs rewards to coverage pool)

- Raise thUSD from the sale of T

I’m going to assume 2. is a non-starter due to complexity in maintaining margin in a DAO.

If we go with 1. the first people who enter the pool stand to gain the most because everyone who deposits after them have to pay the borrow fee (0.5%). That will bootstrap initial liquidity to launch the protocol, however, profits will soon come to an halt after the initial rush of depositors have made their deposits and that could soon after result in liquidity bleed.

The protocol requires ongoing activity (people borrowing, or doing redemptions) in order for profits to be generated. Without LQTY rewards, it’s possible that activity will die down after the initial hype and that will make the APR bad in stability pool, which means people leave with their capital. To accommodate that risk we could instead (according to 3.) allocate less than 100% into the stability pool and allocate some into the PCV. For example 50% into stability pool, and 50% into PCV. Directing some % to the PCV immediately on launch is probably a good idea to establish funds that will not leave the pool even during periods of little activity (and thus profits).

But, if we do some back-on-the-envelope math:

100 million deposited = 500k profit

500k / 2 = 250k

The PCV will be $250k, profit to stability pool depositors: $250k

These are not great numbers. We’d want to have millions in the pool. Even if we went 100% PCV, a meager 500k will not go far.

That leaves us with option 5 & 6. Option 5. is to use T rewards. If we direct T rewards to the stability pool, we will be renting liquidity. Meanwhile we can direct 100% of the profits from lending into PCV. Over time, the PCV will increase in value until a point where we no longer need to issue T rewards.

Option 5. appears like a very flexible and simple option to bootstrap the protocol. But what about option 6.?

The treasury is going to need a 1-2 year runway secured in stablecoins to be able to pay operating expenses regardless of market conditions. This amount can be held as thUSD and placed in the pool (PCV). Funds in the stability pool is very flexible, T DAO can easily draw from the funds when needed. This makes the capital both productive and self-reinforcing. What better stablecoin to store funds in than our own?

How exactly those funds are raised can be debated. Selling T for thUSD on the market, or through some kind of bond mechanism to quickly raise funds with small rebate for purchasers. Amounts are also up for debate, but I will suggest to implement a combination of option 5 & 6.

Numbers

I’m going to make some assumptions here:

- 10% inflation in T

- Price is $0.10 per T

- Target 20% APR

If we allocate 10% of rewards (1% of inflation) to bootstrap liquidity for Threshold USD we can expect to reach $50M in the stability pool.

1% of yearly inflation is worth $10 million. LUSD is considered a safe return, it carries minimal risk compared to other yield farming pools. In fact, liquity has stabilized in the area of 15-25% APR and been there for months.

If we aim for 20% APR we can expect to raise $50 million in the stability pool. Liquity Protocol currently has $853M in stability pool and $1283M LUSD supply. But these numbers are skewed because of the LQTY rewards being so high. It’s not necessary to have that much LUSD placed in the pool for the protocol to survive.

In fact, during the first stress test of liquity only about 93.5M LUSD was offset against the stability pool with 1340m LUSD outstanding. That’s 7%. Some were also recovered through recovery mode. Unfortunately there’s no data on that, but I’ll round it up to 10%.

In other words, $50M in the stability pool should allow for 10x the amount of loans, about $500M. That is plenty of liquidity.

The PCV will grow slowly, for every 1B of loans at least $5M is added to it. But if we can bootstrap some liquidity by having the treasury place some or all of its stablecoin portfolio in the pool we will be able to reduce the amount of T rewards allocated.

E.g if we have a 2 year runway of $25M, placing that in the pool will reduce the T required to half, only 0.5% of total inflation.

These are ballpark numbers and assumptions, I’d be delighted if any statistics/math wizard can crunch the numbers better. But it’s a starting point, and if we’re not happy we have the flexibility to adapt the parameters using the DAO.

My suggestion

- 100% of profits into PCV from day 1

- 100M / 12 = 8.33M T rewards allocated per month to the stability pool (minus whatever treasury puts in the PCV.)

- Gradually decrease T rewards as the PCV grows in size

- Once PCV has grown large enough to support the platform with zero T rewards we can introduce the next phase, which is T-buybacks

- T-buybacks will slowly and gradually increase in percent, e.g it could start as 10% T-buybacks and 90% into the PCV, but gradually increase until T-buybacks are 90-100% of the profit distribution.

T-buybacks can become 100% of the distribution once the PCV is large enough, because the PCV in normal circumstances never will decrease. In fact, we can be expect the PCV to increase even without profits as long as liquidations occur.

During times of high growth it may be necessary to allocate some profits to the PCV anyway in order to keep up with the growth because more positions opened means more can be liquidated during a black swan and that requires more funds in the stability pool. For this reason, we’ll likely never do 100% T-buybacks during growth phases, but stop at whatever makes sense, e.g 90-95%. The % can be voted on by the T DAO.

In summary, replacing the LQTY token results in a much better distribution of profit into useful purposes that can improve the protocol rather than drain it. T-buybacks will take the place of LQTY in times when the PCV no longer need to be funded. T rewards is a temporary stand-in for LQTY in the first months to bootstrap the protocol, with the intention that PCV will take it’s place as soon as possible.

Personal opinion / disclaimer

I’ve been a user of Liquity since inception. I’ve have funds placed in the stability pool. One thing I find particularly amazing about Liquity is that as a depositor in the stability pool, you end up “buying dips” at the most opportune time - that is, when people are getting liquidated.

If you’ve been using DeFi as the price is moving rapidly you know that is difficult due to explosive transaction fees on Ethereum, but when you’re in the stability pool you’re buying ETH at discount without having to spend any money on fees. Imagine having our treasury fund in the stability pool, just gathering rewards effortlessly while simultaneously supporting our own protocol.

Technically you have to withdraw the ETH and sell them on the market yourself, but B.Protocol has developed a system that does this job automatically.

Next steps

While T DAO is not launched yet, I believe we can already start the discussion of this proposal. Most, if not all of it can already be developed and be ready by launch. This is a fork, so the amount of development is not expected to be a lot. But new concepts like PVC and auto-compounding (like B.Protocol) might require some code.

I’m looking for feedback, which ideas are good, which is bad?

Some questions for the community:

-

How much T to allocate to the stability pool

-

How much can the treasury place in thUSD

-

What are your thoughts on PCV vs rented liquidity? Is everyone on board with PCV?

-

Should the protocol’s immutability be preserved? Liquity cannot be upgraded, it has two oracles, one is backup. If we want to add the option of upgradability we should debate a timelock period.

-

What should be the name, do we put this under the same banner as Threshold Network or do we separate the two? I came up with Threshold USD (thUSD) but we can discuss alternatives.

We will also have to consider assigning some liquidity to thUSD pairs on curve, uniswap or similar, but that can be its own proposal.

If anyone is completely opposed to this idea, let your voice be heard. I think this can be a very useful addition to the Threshold Network ecosystem.

This is a soft-proposal. Most parameters can be adjusted by the T DAO as we go along. Quotes for the programming work is something that will have to seek out before we proceed with the final proposal and vote.